Income taken a hit in 2020? Your home equity can plug the gap

If you’re like most older Australians, with some savings in superannuation and relatively fixed expenses, watching your super balance slide in parallel with the stockmarket is like seeing a car crash in slow motion. You want to shout ‘stop’ but you can’t. If you react in panic, you risk making the situation even worse. And you have little control of the outcome or any speed of recovery.

That’s why it’s been such a scary few months for many near-retirees and retirees. Super funds lost as much as 13 per cent of their value in the three months to April 30, according to super research house Chant West, as Covid-19 wrought global economic havoc.

With losses of up to 3.7 per cent, the picture for the 12 months to April 30 is a little better, but that’s not much comfort when the size of your super balance dictates not just when you’ll retire but how well you’ll live in a retirement that might last 30 years or more – every little bit counts.

The super drawdown risk no one talks about

A sharp fall in their super balance isn’t the only worry retirees in particular face when markets are tumbling. There’s another thing called sequencing risk that doesn’t get as much air-time as investment returns but it also plays a big role in whether your super balance lasts the distance.

Sequencing risk is the danger that withdrawals from your super fund damage its long-term returns. Sequencing risk is at its highest when stockmarkets are at their lowest. That’s because if you draw down from your super when investment returns are low or negative (and you’re not still making contributions to your fund to offset those withdrawals), you’re reducing an already shrinking balance.

That means you have less money working for you when markets recover – and that continues to impact the returns you receive over the long term. In short, your overall investment performance often fails to recover from those drawdowns during stockmarket slumps.

To help retirees minimise their sequencing risk, in March the government cut the minimum drawdown requirements applied to super income-stream products. The usual minimum drawdown rates range from 4-14 per cent of your super balance, depending on your age. But for 2019-20 and 2021-22, those rates have been cut in half, to 2-7 per cent. The idea is that drawing down a lower sum better preserves your balance while you wait for markets to recover, thus reducing the sequencing risk impact.

But what if you can’t postpone retirement until your balance has recovered enough to produce the income you’ll need? Or if you can’t slash your expenses in retirement to match a lower drawdown rate?

That’s the issue that Marilyn, whose name we’ve changed to protect her privacy, faced. A self-funded retiree who’s reliant on income from her super and a residential rental property to fund her retirement, she was worried about the losses her super balance showed after the Covid-19 market rout but having settled into a retirement lifestyle over the past four years, didn’t want to make substantial changes to her budget.

“My super was hit hard with the market drop so I didn’t want to continue to draw down from it while it was showing a big loss,” the 69-year-old told Starts at 60. “I have an investment property that I receive income from too and the tenants have so far been very good tenants and have never defaulted on payments but you just don’t know what will happen in this volatile situation.”

Using home equity to protect your super balance

If you’re in a similar situation, a solution you may not have considered is a reverse mortgage, which is a way of releasing equity from property to use as income.

Household Capital is an Australian company run by top financial experts, that specialises in helping older Aussies use their family home to cover short- or long-term shortfalls in their retirement income through a product called a Household Loan.

A Household Loan lets you use your property as security against a loan that doesn’t have to be repaid until you sell the property (although you can pay off the loan at any time with no penalty). Your loan can be paid as a lump sum or as ‘Home Income’, of fortnightly or monthly instalments – or both – making it an ideal replacement for a regular super income.

Josh Funder, the CEO of Household Capital, says he’s seen a jump in interest in Household Loans from retirees who’re concerned that now is the wrong time to draw down on their super but still need to create or supplement an income stream (with or without the Age Pension) so they can keep paying their bills comfortably in retirement.

“We’ve experienced increased interest in Household Loans, particularly from self-funded retirees who’ve found their retirement income affected by Covid-19, including people relying on rent from commercial property, retirees with share portfolios and people not wanting to draw on their super while the balances are negatively impacted by the market,” he says.

“We also hear from people who are getting little from the funds they’ve got in cash and are fearful about falling dividends so need to supplement those income sources.”

With the average Aussie super balance of an 60-64-year-old sitting at $154,452 for men and $122,848 for women, many people could hugely increase the money they have to hand – some by up to 400 per cent! – according to Household Capital calculations.

And whether they use a Household Loan to prop up their finances just while they wait for markets to make a comeback, then start or resume super drawdowns, or use the loan as a long-term income solution is up to them, Funder says.

“Plus, using their home equity and leaving their super or investments to recover, can help retirees avoid sequencing risks,” he adds.

Marilyn is one of the retirees who approached Household Capital in search of a way of replacing the income from her super fund while she waited for markets to recover.

“A friend has a reverse mortgage and I saw that it works as a good option for people who’re not eligible for a government pension,” she says. “It just means I have more flexibility in my options and it’s very reasonable because I retain my home, my investment property and my super – my Household Loan is just like an emergency measure to act as a buffer.”

How a Household Loan can stretch your super further

Marilyn is a great example of how such a loan can help Aussie retirees. Aged 69, she’s confident that given time to bounce back from the current market doldrums, her super will see her out. But the $20,000 lump sum plus monthly Home Income payments of $2,000 she took as a Household Loan will give her the breathing space she needs to allow a stockmarket recovery to occur.

Plus, she’s making monthly interest-only repayments so the total size of her loan doesn’t increase over time due to compound interest.

“I estimated how much I’d need to pay bills over the next few months, so settled on a lump sum that was more than what I needed, and then what I’d need to pay bills over, say, five years and I applied for what’s a modest amount in total compared to the value of my property,” Marilyn explains. “The Household Loan gives me peace of mind and more flexibility in my financial options.”

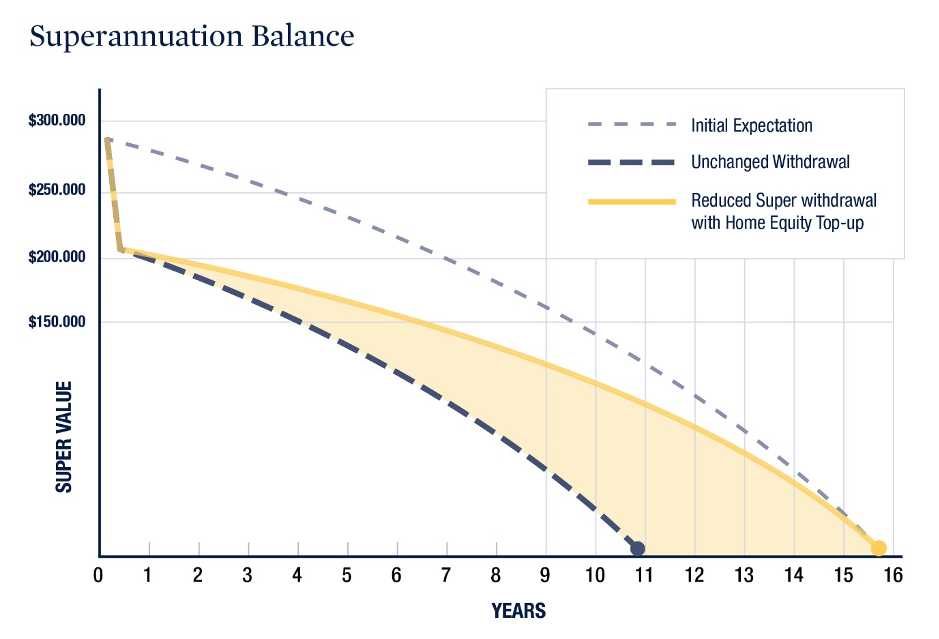

The case study below helps demonstrate how reducing super drawdowns with an income boost from a Household Loan can make a significant difference to how long your super lasts.

Picture a 65-year-old couple with $280,000 between them in super and a house they own outright that’s valued at $900,000 (not at all out of the realms of possibility given the Australian domestic property had a mean price of $691,000, according to the latest data). The couple draw an income of $2,000 a month from their super and receive $2,847.20 a month from the pension.

They want to ensure their super lasts as long as possible, so are keen to keep it invested so they can benefit from a stockmarket recovery. But they don’t want to sacrifice the retirement lifestyle they worked hard to achieve.

If the couple keeps drawing a $2,000 monthly income from super, their super runs out by the time they’re 75 and they’re down to living on the pension alone. If they cut their expenses – goodbye regular travel, car upgrades or home improvements – and reduce their monthly super income to $1,500 a month, their super lasts until they’re 80.

But if they reduce their monthly super income to $1,500 and top it up with a $500 monthly Home Income payment, they can still stretch their super out until they’re 80 but maintain their current lifestyle.

You might think this would eat up a big chunk of their home equity, but it requires just a $90,000 Household Loan. The sum repayable at the end of the 15-year loan term would be about $136,000 in total due to compounding interest – not a large bite out of the couple’s total home equity of $900,000 (and that’s assuming their home doesn’t increase in value at all over the 15 years).

You can see in the chart below how a Household Loan can help super last for longer (and that’s assuming their super investments don’t increase in value at all over the 15 years either).

Whether you’re like Marilyn, whose Sydney home is worth more than the couple in the case study, or have a property worth a more modest sum, Household Capital can work with you to create a solution that suits your personal circumstances.

You can find out more about Household Capital here but it’s important to consider Marilyn’s advice too.

“I think there are pitfalls to reverse mortgages if you don’t do your research,” she says. “I had looked at another company offering reverse mortgages but when I showed my lawyer their documents, he found a lot of questions that weren’t clear and issues that weren’t clarified – just a lot of gaping holes in their proposition – so he recommended I look at Household Capital and sent me away to do more research.

“When I looked into it further, I saw that Household Capital was just very straightforward in how it set out a plan for me. So I think it’s important to know the difference between what companies are offering because they may say that they’re all offering a reverse mortgage but they’re not all the same.”

HOUSEHOLD CAPITAL INFO Important information. Applications for credit are subject to eligibility and lending criteria. Fees and charges are payable, and terms and conditions apply (available upon request). Household Capital Pty Limited is a credit representative (512757) of Mortgage Direct Pty Limited ACN 075 721 434, Australian Credit Licence 391876. HOUSEHOLD CAPITAL™, the Star Device and Household Capital and the Star Device are trademarks of Household Capital Pty Ltd.

IMPORTANT LEGAL INFO This article is of a general nature and FYI only, because it doesn’t take into account your financial or legal situation, objectives or needs. That means it’s not financial product or legal advice and shouldn’t be relied upon as if it is. Before making a financial or legal decision, you should work out if the info is appropriate for your situation and get independent, licensed financial services or legal advice.

Whether your home needs reroofing, your mortgage needs refinancing or your teeth need recapping, your home equity can renew your retirement and help you enjoy the lifestyle you deserve. Try our easy-to-use calculator to see how much home equity you could access.

Proudly Australian owned and operated

Proudly Australian owned and operated