Property investment: Your essential ‘sell or hold’ checklist

I have reviewed a number of questions from Starts at 60 community members recently about residential rental property and retirement. Typically, the questions, such as this one, were around whether to retain or sell the property and put more money into super.

As such, I thought it would be worth undertaking an analysis to determine whether or not (on average) it makes sense for retirees to retain residential rental properties in their investment portfolios. I will focus here on an analysis of the broader market but must acknowledge that there is no substitute for undertaking an analysis of individual property holdings before making any decisions.

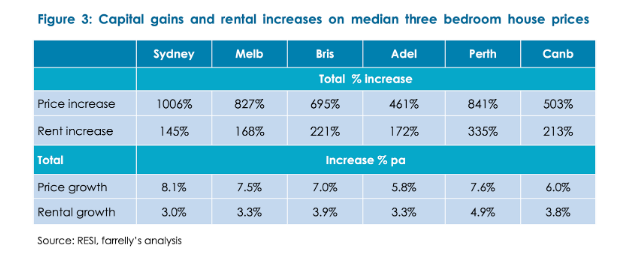

I recall an excellent analysis of the residential property market by Tim Farrelly, undertaken a couple of years ago. His chart below, which shows changes in property prices and rental returns since 1985, is very revealing.

The chart shows that across the major capital cities, there has been a dramatic increase in prices of houses but that has not been matched by rental returns. The rate of increase in house prices is more than double the increase in rental returns. As a result, the average yield on rental properties has fallen dramatically as prices have increased.

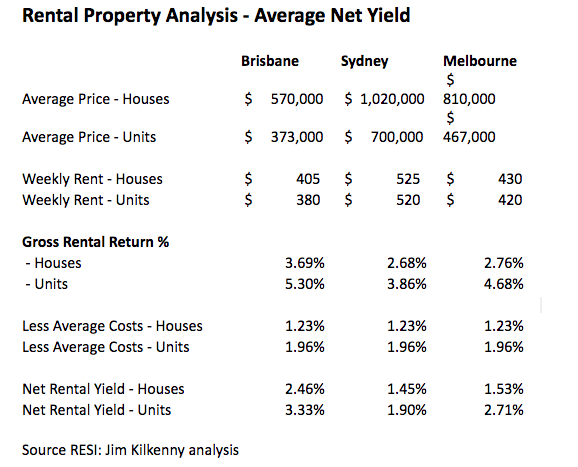

As the analysis above was done two years ago and house prices have fallen and then recovered somewhat in that period, I have undertaken a further analysis using the current median house prices and median rents, which are shown in the table below.

You will see from the table above the net rental returns for houses and units across the three major capital cities. The net rental return calculation allows for the average cost of owning a property and includes all the normal costs plus allowances for agents’ fees, periods of vacancy and costs of renovations over time.

How property stacks up against other assets

The average net rental yield for houses is 1.81 per cent and for units is 2.65 per cent. Of course, the situation for individual properties will vary as will the situation from city to city and town to town, as is apparent from the table above.

Based on this analysis, house prices are approximately 50 times the net rental return they generated and units are 37 times. This multiple can be compared to the price-earnings (PE) ratio of the sharemarket, which is currently between 17 and 18 times.

In simple terms, this means the price of the average house is around 50 times the net rent whereas the average price of shares of Australian companies is around 18 times the dividends paid (average dividend yield is 4.30 per cent, excluding the benefit of franking credits).

So, purely based on the amount of income, the average house or unit produces a relatively low income return compared to shares but at present is still significantly better than cash and term deposits. Also, the price multiple for houses and apartments is substantially greater than Australian shares or international shares for that matter. On this measure, houses and units look expensive!

Sell or hold your property? What to consider

Clearly, the key driver for owning real estate will not be the net rental return but the potential for capital gains.

However, the last few years shows that the trend in price growth is not always up. Furthermore, historically low interest rates have continued to prop up residential property prices and potential increases in interest rates in the future will need to be watched carefully.

So, what else does a retiree need to consider on whether to buy or hold or sell residential property as part of their investment strategy in retirement? Personally, I believe you need to consider the following:

Liquidity

Residential real estate is an illiquid asset and cannot be easily converted into cash. Furthermore, there is no option to dispose of part of your holding to generate cash as you can only sell the entire asset – you can’t sell off the front porch. An alternative is to borrow back against the property, however, for a typical retiree borrowing to invest does not generally make sense as tax is often a non-issue and the costs of borrowing often exceed the benefit.

Diversification

Another issue the residential property is the concentration of investment in a single asset. Unless you’re in the fortunate position to own several residential properties in different geographic locations, residential property holdings typically reduce diversification for an investor and thus increase risk.

Borrowing

A high proportion of residential rental properties in Australia are geared. The alleged tax benefits of negative gearing have been a strong attraction for investment in these assets.

I would normally recommend that retirees do not have borrowings as part of their investment strategy. You will see from the table above that the net rental returns are still less than current borrowing rates even at today’s historically low levels. Accordingly, if you are retired or about to retire you will need to have a strategy for managing the debt on your residential property and sometimes selling to clear the debt is the only option.

Management

Many landlords will utilise an agent to manage their property and this can be sometimes frustrating and expensive process. Even with an agent, there are still significant decisions to be made by landlords such as repairs and renovations, problem tenants, vacancies and so on.

Also, as an owner ages and may live remotely from the rental property, these decisions can become very difficult.

Holding costs

Compared to other asset classes, the holding costs of residential property are very high and need to be carefully managed over time in order to avoid impacting too greatly on net rental returns.

Buying and selling costs

Relative to other investment choices (shares, for example) the costs of buying and selling rental properties are very high including agents’ commissions, stamp duty and legal fees.

The information above provides a summary of the key issues that need to be considered by retirees, however, as usual the decision for each individual will depend upon their particular circumstances, needs and objectives. I believe there are sensible reasons to buy and retain residential property, however, these reasons need to be constantly reassessed over time as individual circumstances change.

Retirement is one of these times. I am now retired and I now have no residential rental properties and have focused on commercial property only. The rest of my investments are highly liquid and spread across all asset classes to provide diversification and cash flow.

Proudly Australian owned and operated

Proudly Australian owned and operated

Comments 0

Join the conversation. Comments are reviewed before they appear.

Be the first to comment.

Join the conversation

Tell us who you are to post a comment. We'll remember you next time.