Starts at 60 fans who are struggling to make ends meet could be popping the champagne corks in a few days, with sizeable increases in Centrelink eligibility thresholds to kick-in from July 1.

Thousands of Starts at 60 readers are likely to qualify for a pension for the first time and those already on a part-pension, could see some sizeable increases in the rate of pension payable.

In some cases, the increase could be as much as $2,223 per year.

The increases come on the back of July 1 indexation of Centrelink means test thresholds which continue to benefit from Australia’s escalated inflation rate.

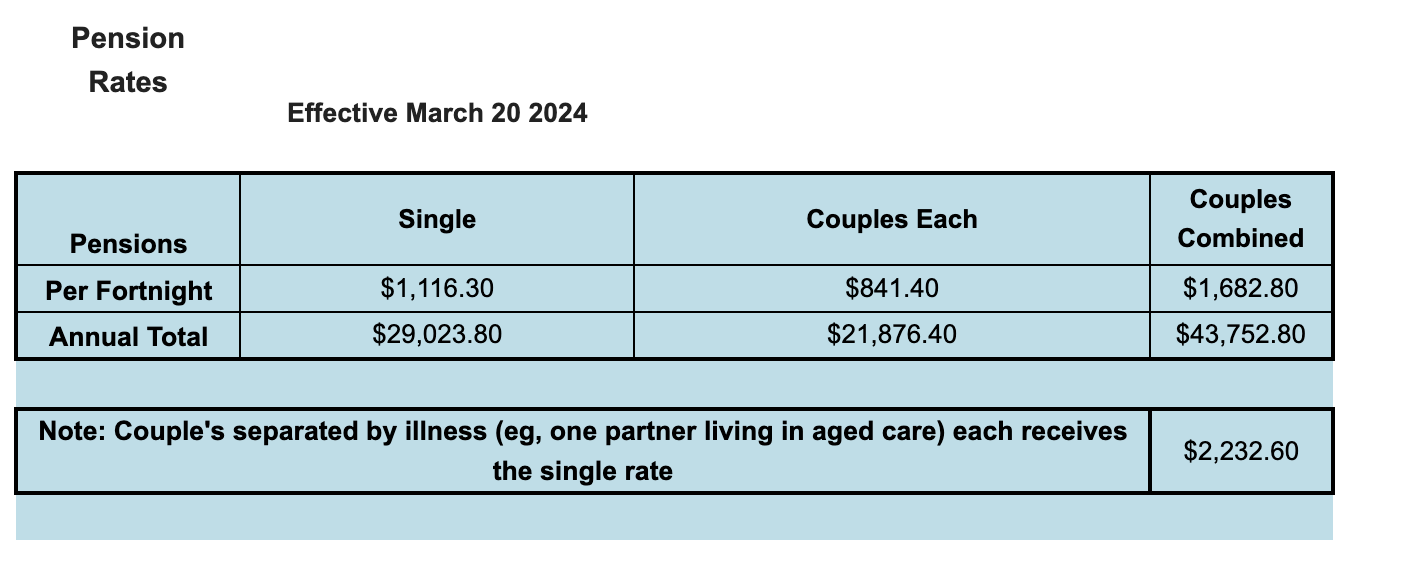

Pensioners already receiving a full pension won’t see any change. Their next increase for them will arrive on September 20 and at this stage, we don’t know by how much.

Under the means testing system, pension eligibility is tested against income and assets and whichever test produces the lowest pension payable is the one used. A person could pass on one test and fail on the other.

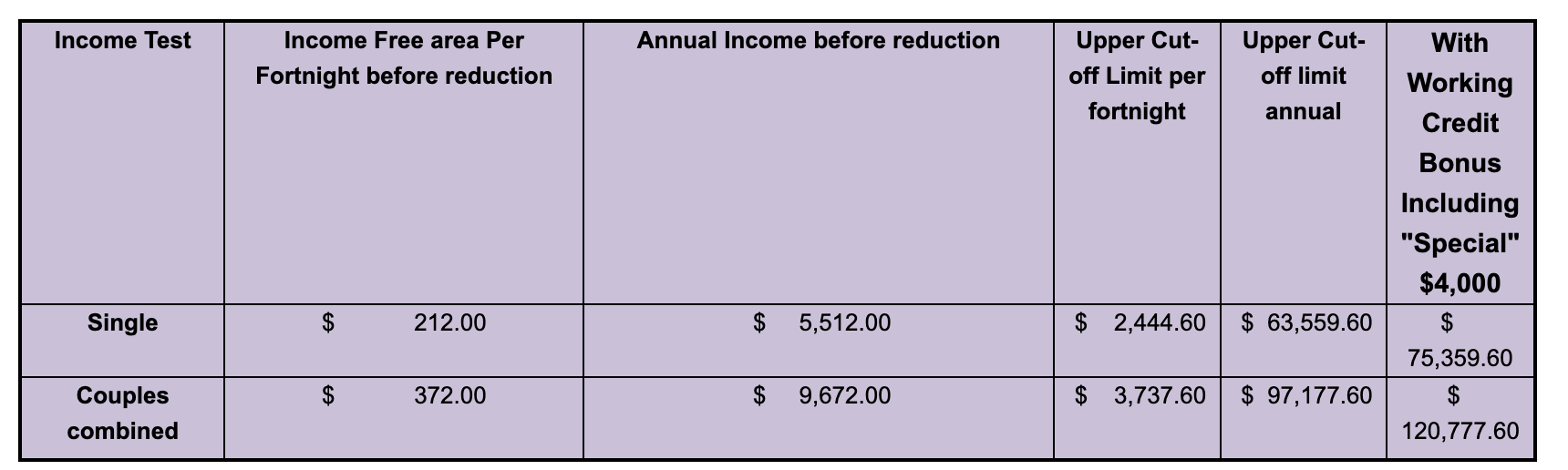

Under the income test from July 1, Centrelink assessable income which exceeds $212 a fortnight for singles, sees the full pension of $1,116.30 per fortnight clipped at the rate of 50 cents per dollar until it is cancelled altogether. That happens when income exceeds $2,444.60 a fortnight.

This is an $8 per fortnight increase from the current income free area of $204. Don’t get too excited though, the maximum increase attributable to this change is $4 a fortnight. Not even enough to buy a coffee these days!

For couples, the new combined income free area of $372 is a $12 increase on the current level of $360. The full pension of $841.40 per fortnight each, will cut out when combined income exceeds $3,737.60. Again, the maximum increase for couples under this change will be a whopping $6 a fortnight. You can now buy your coffee, but you’ll have to share!

Pensioners who continue working have an additional $300 a fortnight added to their income free area before the pension starts to get clipped. In the case of couples, each pensioner can access the extra $300 but you can’t share it with your partner.

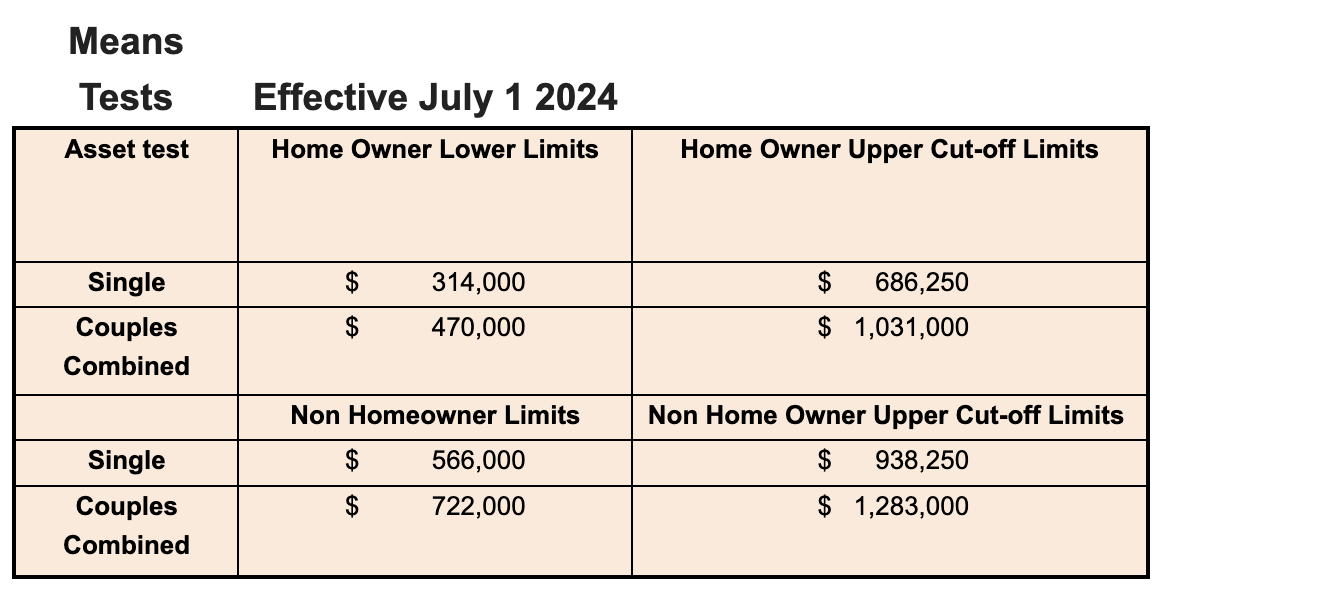

But by far the nastier of the two means test is the asset test. It’s also where you’ll see the biggest increases from July 1 because an increase in the thresholds means a decrease on the effects of the asset test.

For a single home-owner from July 1, once Centrelink assessable assets exceed $314,000 the full age pension starts to be reduced at the rate of $3 per fortnight per thousand dollars over. The pension gets cancelled altogether once assets exceed $686,250. This is an overall increase in the asset test threshold of $12,250.

For home-owning couples, an overall increase of $18,500 means the new lower limit will be $470,000 but the upper cut-off limit will be a whopping $1,031,000. Remember, your private home no matter how much it is worth, is exempt from the asset test.

Non home-owners whether singles or couples, will be allowed an extra $252,000 in assets before the asset test starts to bite.

The significance of these changes is that if nothing has changed and you are on a asset tested part pension from Centrelink, you’re likely to see an increase on July 1.

For example, the $12,250 asset test increase for a single asset tested part-pensioner means the current $3 per fortnight reduction will be reduced by the effects of the increase.

In this case, the pension would rise by 12.25 X $3 or an extra $36.75 a fortnight, unless you reach the maximum pension payable or the income test takes over.

A non-home owning asset tested couple benefits from the effective increase of $28,500 in the asset test threshold. At $3 per thousand, that translates to an extra $85.50 a fortnight. Over the year, that adds up to at least $2,223.

Remember that between now and July next year, there will be two increases to the amount of pension payable . That happens in September and March so over the full year, these increases will be even higher.

One final point. If you benefit from the changes under one test, keep your eye on the other. It could be that the other test now takes over as the dominant means test used in calculating your pension.

The new means test thresholds applicable from July 1 2024.

![]()

Proudly Australian owned and operated

Proudly Australian owned and operated