Hot off the press for Starts at 60 readers, we have the new increased Centrelink means test thresholds. While many part-pensioners will receive an automatic increase on July 1, it also means that thousands of Aussie seniors will be entitled to Centrelink Benefits for the first time.

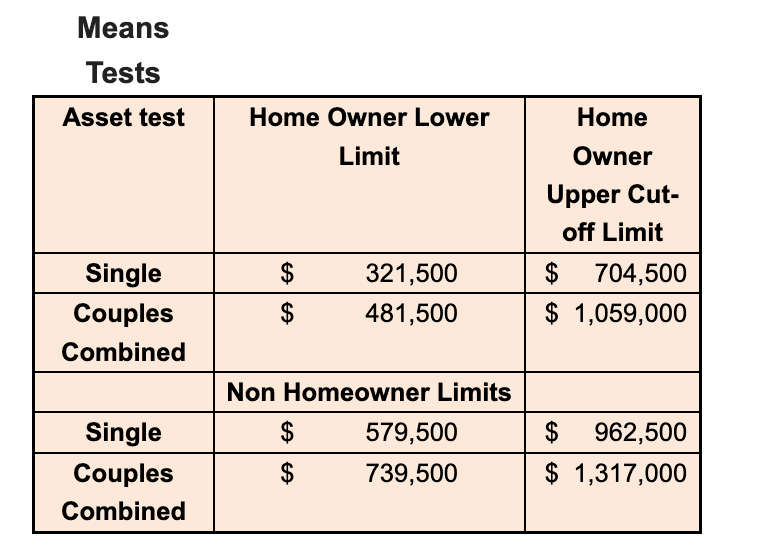

The changes, set to apply from July 1, will see a home-owning couple eligible to receive a part-pension if their combined Centrelink Assessable annual income is just under $100,000 and their assets, excluding the family home, are under $1.059 Million.

That also means access to the highly sought after Pension Concession card, which could be worth up to $7,000 in savings for some households, depending on which state you live in.

The legislated increases are tied to Australia’s Consumer Price Index and will apply until July 1, 2026.

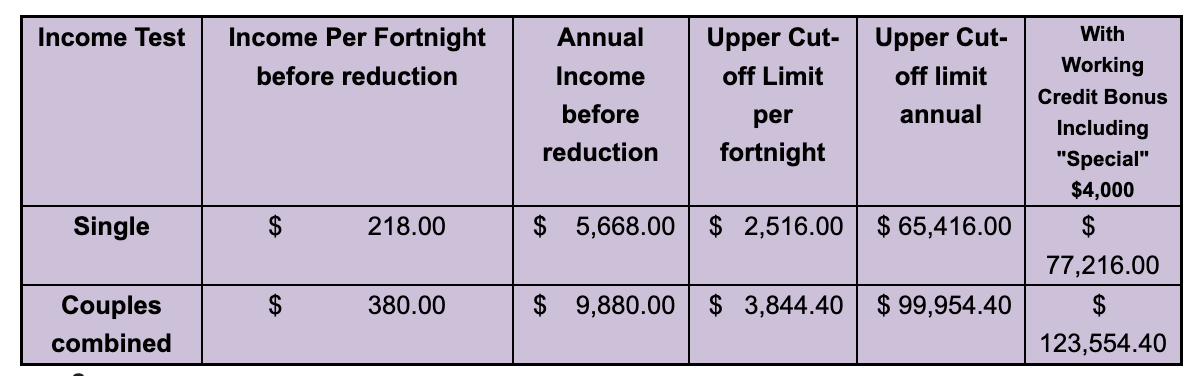

From July 1, singles receiving an Age or Disability pension and those receiving a Carer Payment will have a Centrelink assessable income free area of $218 per fortnight, an increase from the current level of $212. Under the Income Means test, each dollar over the threshold, reduces the pension by 50 cents per fortnight until it hits the new upper cut-off limit of $2,516 per fortnight.

For couples, the new combined income free area will see an $8 increase to $380 per fortnight with an upper cut-off of $3,844.40 per fortnight.

Centrelink regards couples as a single entity so effectively, the income could all be earned by one member of a couple.

Again, a 50 cent per dollar reduction applies to the combined pension payable, if the income test threshold is exceeded.

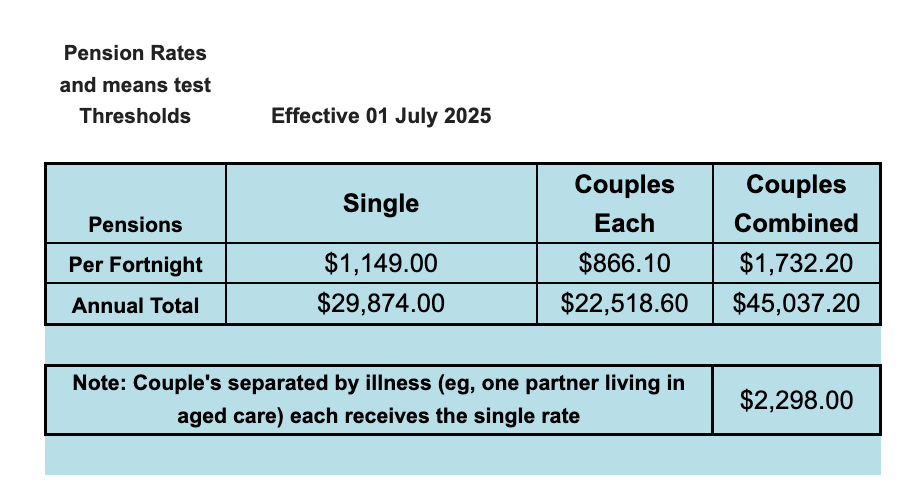

If you’re currently an income-tested pensioner, that will be an automatic increase of $3 a fortnight for singles and a combined $4 a fortnight for couples. Not much, but every little bit helps.

Centrelink assessable income is not the same as taxable income or cash-flow.

Instead, Centrelink includes gross employment income, net rental income, foreign pension income and apply a deemed rate of interest to all financial investments to determine Centrelink assessable income.

The deeming rate thresholds also increase to $64,200 for the lower threshold for singles and $106,200 for couples. Under current deeming rates, a deemed rate of interest of 0.25 percent applies up to the lower threshold and then a rate of 2.25 percent applies to all financial investments above the threshold. That annual figure is converted to a fortnightly amount and applied towards the fortnightly income free area.

Income from employment for Age Pensioners and Career Payment recipients also receives a further exemption of $300 per fortnight. That means for example, a senior with part-time employment and other assessable income could earn up to $518 per fortnight before seeing their pension reduced under the income test.

By far the harshest of the two tests is the Asset means test. Under the Centrelink system, whichever test produces the lowest pension is the one Centrelink will latch onto.

For a home-owner, the entire value of the home is ignored, providing it is used by the Centrelink customer for private purposes and sits on less than 2 hectares.

The lower threshold for a single home-owning pensioner increases from $314,000 to $321,500 and for a couple, from $470,000 to $481,500. This also lifts the upper cut-off threshold for a home owning single from $697,000 to $704,500 and for couples, to a whopping $1,059,000.

Simply because of the increase, an asset tested single should see an automatic increase in their fortnight pension of $22.50 and for couples a combined lift of $34.50.

Under a quirk in the system, those just under the upper cut-off threshold will receive at least $59.10 per fortnight if a single and $44.50 each for eligible members of a couple if residents of Australia.

This is because the full fortnightly payment includes the base pension plus supplements to cover the costs of communications, prescription medicines and energy. While the legislation allows the base pension to be steadily reduced, the supplement payments are made in full, or not at all.

That also entitles the part-pensioner to receive the treasured Pension Concession Card which entitles holders to receive substantial discounts on State and Federal government utilities and services.

The Association of Independent Retirees have previously identified that when combined with private discounts and depending on which state you live in, in some cases, these savings could be more than $7,000 per annum.

Non home-owners both singles and couples, are allowed an extra $258,000 in assets before their pension starts to reduce under the asset test.

Payment rates increase twice per year in March and September and these will have an effect of lifting the upper cut-off thresholds even higher.

Starts at 60 will have these for you, as soon as we know.

IMPORTANT LEGAL INFO This article is of a general nature and FYI only, because it doesn’t take into account your financial or legal situation, objectives or needs. That means it’s not financial product or legal advice and shouldn’t be relied upon as if it is. Before making a financial or legal decision, you should work out if the info is appropriate for your situation and get independent, licensed financial services or legal advice.

![]()

Proudly Australian owned and operated

Proudly Australian owned and operated